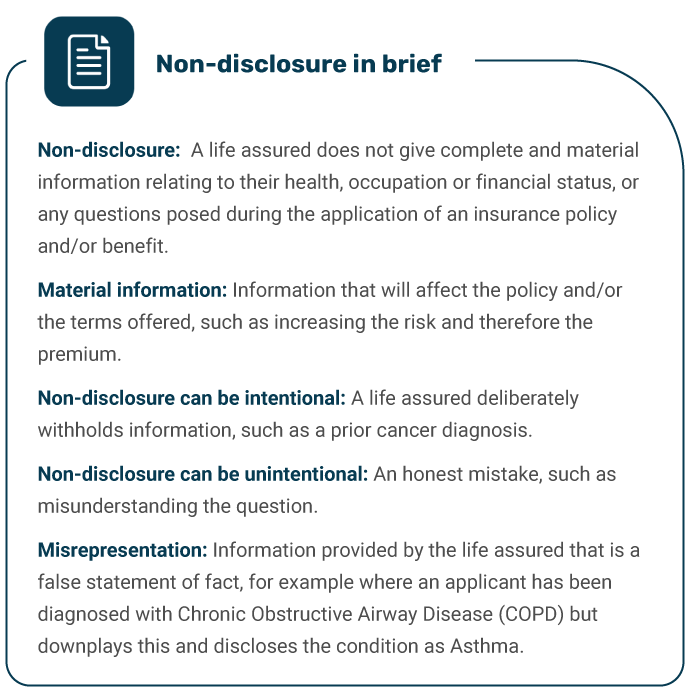

Deliberate non-disclosure of material information will result in declined or reconstructed claims, leaving families without the funds they need. Advisers have a critical role to play when it comes to preventing non-disclosure. With their expertise, insight and patience, they can help clients disclose all material information and avoid the trauma of a declined or reconstructed claim.

Over two-thirds of fraudulent and dishonest claims involve non-disclosure or misrepresentation

South Africa’s life insurance industry has a stellar payment record – paying out billions of rands for well over 95% of claims (+99% in 2020). However, claims are declined or reconstructed when fraud and/or dishonesty is detected. In over two-thirds of fraudulent and dishonest claims, non-disclosure or misrepresentation is involved.

A claim is reconstructed when it is based on different cover or sum assured than the original cover offered. For example, if life cover of R1 million was granted at standard rates originally, and non-disclosure of a chronic illness was detected at claims stage, the original offer for cover would have changed and a loading applied to the premium if the illness was disclosed. The claim for the R1 million would then be reconstructed as claim for a lower amount based on what the premiums paid would have covered, for example R700 000 instead of R1 million.

In 2021, 305 fraudulent and dishonest death claims, worth a staggering R238 million, involved misrepresentation or material non-disclosure. This represents two-thirds of all fraudulent and dishonest death claims. 68% of fraudulent and dishonest funeral claims, 2 232 claims, were found to have involved misrepresentation or non-disclosure. The numbers are higher for disability claims where 94% of fraudulent and dishonest claims were found to have been due to misrepresentation or non-disclosure. These statistics from the Association of Savings and Investment South Africa (ASISA) show that non-disclosure is a problem, and in areas such as funeral cover, it is increasing.

The impact of non-disclosure is felt when claims are declined or reconstructed and families suffer financial loss or even poverty. There can also be reputational damage to all parties, no matter what the facts of the case.

Help your clients disclose all material information

No one wants to spend too much time filling in forms. But you and your clients do have to make sure everything is clear and answered accurately and completely.

1Life’s underwriting and client service teams shared these tips to help advisers ensure clients disclose all material information upfront.

1. Take time to complete application forms

It is well worth spending a few extra minutes explaining the questions and terms on forms in detail, and giving clients time to think about the questions and their answers to ensure there is full disclosure. An insurance policy is a legal contract that comes with the terms and conditions. Explain this to your clients and emphasise the importance of not rushing the application process, and the consequences of not disclosing - either deliberately or by mistake.

2. Know the products and forms

To help your clients understand all the questions, YOU need to understand them. Always go through forms regularly to make sure you understand and can explain exactly what information the insurer is looking for. Attend training sessions your product provider holds, and ask for more training or explanations if you are unsure of anything.

1Life hosted a series of workshops with forensic experts to help advisers help their clients disclose all material information. Your consultant will have more information on this and any upcoming training and workshops.

3. Avoid rephrasing or summarising questions

In a case reported in the Long-term Insurance Ombud’s 2021 Annual Report, medical questions were said to have been asked in a “generic fashion and not read from the application form”. This resulted in information not being disclosed, and a declined claim being referred to the Ombud. Avoid restating questions and rather explain them. For example, if a question asks if a client has experienced chest pain, explain that this means any chest pain, and avoid asking if the client has had a heart attack.

4. Be wary of catch-all questions

A specific question such as “have you ever had pneumonia?” is easy to answer. A general question such as “have you ever had a respiratory illness?” is not so easy to answer. They are very different questions, and advisers and clients need to understand the differences. The one refers to a specific condition or illness, the other broadly to any ailment affecting the respiratory system. The idea here would be to explain what the respiratory system is, and give some examples of conditions and illnesses. However, be careful of limiting the client to only one example – they need to know there is more than one.

5. Be clear about occupation questions

These help underwriters determine risk and premium, and inaccuracies can lead to reduced pay-outs or declined claims. Have your client explain what they do for a living, and when and where they work, so the correct occupational risk is recorded.

6. Ask product providers for clarity and updates to forms

Sometimes, forms will provide a list of options that your clients believe do not reflect their true answer. This can apply to a job type, a medical condition or even the frequency of, for instance, travel. It is critical to tell your product providers when you and your clients have difficulty with questions or when the answers to questions do not fit prescribed responses so they can update their forms.

7. Make sure clients know that having a medical condition doesn’t disqualify them from cover

Clients are often wary of parting with the whole truth because they fear it will mean their application won’t be accepted. They need to be assured that this is simply not true. Instead, these kinds of questions will mean that the client receives the right cover at the right price. For some higher risks, premiums will be loaded, but not all medical conditions will come with higher premiums. In certain cases, based on an applicant’s risk profile, cover may be declined and accidental death benefits may be offered.

An excellent example is Asthma. 1Life offers cover for asthmatics, and if the disease is well controlled premiums are reasonable.

Make sure your clients are paying for benefits that will be paid

If a client doesn’t disclose information when taking out a policy, they are wasting their money, as they will be paying for benefits they won’t qualify for. Financially, non-disclosure is a bad decision. Advisers can help their clients make the right financial decisions by helping them fully disclose all relevant information at the application stage.

The information contained in this article was correct at date of publication