Life insurance is designed to protect your dependants from financial ruin if you can no longer provide for them. If your beneficiaries are minor children, under the age of 18, there are a few extra steps you need to take to make sure your minor beneficiaries will benefit.

1. Name your children as beneficiaries

If you want your insurance policy to benefit your children, name them as beneficiaries. Be specific when you name beneficiaries – give full names and ID numbers.

2. Name a guardian for your children in your will

Biological parents are legal guardians, so if one parent dies the other parent is legally required to care for their children. But in the event of both parents passing away, name a guardian, a close relative or friend, who will care for your minor children.

Should you not name a guardian, the High Court will appoint one.

The guardian cannot receive the proceeds of an insurance payout unless you have named them as beneficiary and to do this you would have to be 100% confident that they would use the money wisely, as you intended, for the care of your children.

If you do not want the guardian to be your beneficiary, set up a trust for your children to ensure they benefit from the proceeds of your life insurance.

Top tip: Apply today for the Truth About Money and LIPCO’s wills and estate benefit. LIPCO will help you draft a will for yourself and your spouse or set up a trust for minor beneficiaries. You can also apply for legal advice and mediation if you need help winding up the estate of a relative.

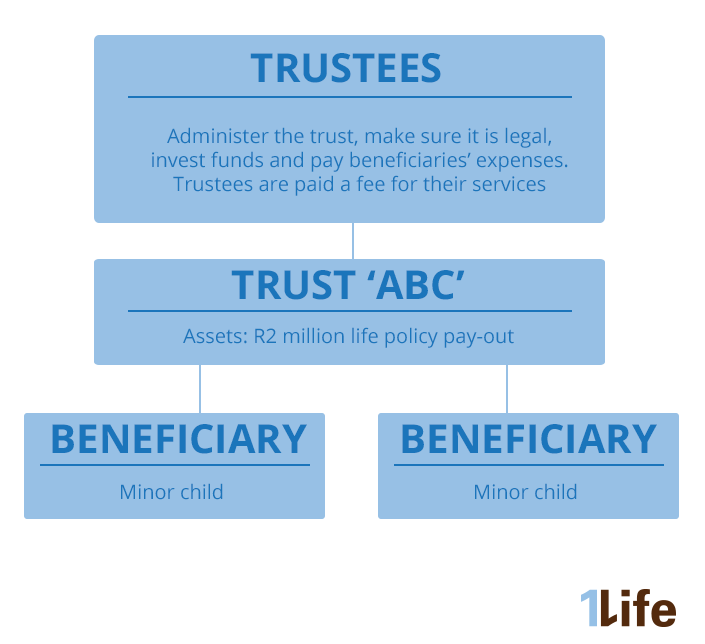

3. Set up a trust in your will that will administer insurance pay-outs for your minor children

A trust is a legal entity that holds assets for the benefit of another. So a trust will hold the proceeds of your policy and invest or administer it for the benefit of your minor children – paying for school fees, extramural activities, clothing and so on.

Use an expert to set up a trust

Trusts are legal documents subject to a number of rules and regulations and it is highly recommended that you use an expert. You can ask a financial advisor or lawyer for assistance, or contact the Fiduciary Institute of South Africa.

There will be a cost involved in setting up the trust but it will allow your minor beneficiaries to benefit as soon as the claim is paid out.

Name the trustees

These are the people who administer the trust and invest and distribute funds. Ideally, there should be at least one independent trustee to provide an objective overview. An independent trustee won’t have anything to gain or lose financially from managing the trust.

the guardian may be fantastic with your children but not as good with money management.

The guardian of your children can be a trustee, but doesn’t have to be, and most experts recommend that the guardian is not the only trustee. The reason – the guardian may be fantastic with your children but not as good with money management.

If there is no trust set up, and your beneficiaries are minors, the proceeds from your life insurance will be paid into the Guardian’s Fund, which is a fund set up by the Master of the High Court that administers money on behalf of minors, dependant adults and unknown or untraceable beneficiaries.

The Guardian’s Fund is managed according to strict guidelines and limits the amounts minors can receive - for example only R250 000 of the capital amount. If you have life insurance of R2 million, and your children are in private school, this amount may not even cover their fees. A trust is not subject to these limitations. If you want your children to benefit from the full amount when they are minors, a trust is the better option.

Setting up a trust may seem like a lot of work, but they offer flexibility and accessibility. If you are concerned that trusts are expensive, look at the advantages and decide if they outweigh the costs.

Trusts versus the Guardian’s Fund

| Trust set up in terms of will | Guardian’s Fund | |

| Managed by | Trustees you have selected | Master of the High Court |

| Investments | Trustees have flexibility and discretion where they invest, unless specific guidelines have been set out in the trust deed |

Funds are invested with the Public Investment Corporation |

| Investment return | Flexible – depends on where the funds are invested | Fixed – the rate of interest earned is set by the Minister of Finance and reviewed from time to time – the current rate is 9% |

| Funds can be used for | A variety of purposes, the trustees decide how much can be used and when | Maintenance purposes only, such as education, medical expenses and clothing |

| Access to funds | No limits unless set out in the trust deed | A maximum of R250 000 of the capital amount can be used, and all the interest earned. Let’s say your life insurance paid R2 million to your beneficiaries, they would only be able to use R250 000 until they reach 18 years. All the interest earned can be used. |

| Admin and procedures | Trustees are easier to access but will require supporting documentation, like an account for school fees to make sure the trust pays legitimate expenses and keeps a record of how the funds were spent |

Can be ‘cumbersome’, time consuming and require the filling out of forms and comprehensive documentation |

|

Age of majority when the |

18 or higher – you can stipulate that the full amount can only be accessed at 21, for example | 18 |

Trusts have a major role to play in the financial care of minors and are widely used

You may have heard that trusts are going to be taxed at higher rates in the future and are not worth the time and effort. This is unlikely to be true for all trusts, particularly those that are set up to protect minors and special needs dependants.

Leaving the proceeds of an insurance policy to an estate

Setting up a will naming your children as your heirs, and naming your estate as the beneficiary on your insurance policy might seem a logical alternative to setting up a trust for your children. There are three reasons why it might not be the best option:

- Proceeds paid into an estate form part of the estate and anyone who has a claim on that estate will share in the proceeds. So, if you had a mortgage bond that needed to be settled, some of the proceeds of your life insurance could be used for that purpose.

- Once funds are part of your estate, distributing them incurs executor’s fees, and possible estate duty.

- Estates can take a long time to settle and you can wait for funds for over 12 months. And once the payments are made, they will be paid into the Guardian’s Fund if the beneficiaries are minors.

Closing thought

If your beneficiaries are minors, consider setting up a trust – it will save time and allow access to funds as quickly as possible. Use an expert to make sure your trust is correctly set up and complies with all the legal requirements.

The guardian may be fantastic with your children but not as good with money.